What is debanking?

Debanking is when a bank, card processor, or payment provider terminates its relationship with a customer — closing accounts, freezing balances, or refusing service — often with little warning and no real explanation. The business has not broken any law. It has simply been judged too risky, too much trouble, or too far outside the provider's comfort zone to keep. For an individual it is an inconvenience; for a business it can be existential, because no account means no payouts, no payroll, and no supplier payments. And because financial providers rarely explain themselves, most debanked merchants never learn the real reason.

Why do banks and processors debank legal businesses?

- Risk and compliance cost. Some industries trigger extra anti-money-laundering scrutiny. Rather than do the work, providers often just exit the relationship.

- Reputational risk. A vague catch-all that lets a provider drop you for who you are or what you sell, even when it is perfectly legal.

- Chargebacks and disputes. A dispute rate that drifts toward 1% can flag your account for offboarding.

- Politics and pressure. Regulatory signals and public pressure push providers to pre-emptively cut off entire categories — see Operation Choke Point 2.0.

How is debanking different from a normal account closure?

A normal closure comes with notice and a reason. Debanking is abrupt and opaque: a templated email, a frozen balance, and a support team that will not say more. That opacity is the point — it removes any path to appeal. Practically, that means you cannot rely on warning or a chance to fix things; the safer assumption is that it can happen with no notice at all.

What to do if you are debanked

- Screenshot every notice, balance, and message as your record.

- Move any accessible funds to a separate institution.

- Ask for the reason in writing, even if you may not get a clear one.

- Stand up a payment rail that does not depend on a bank account, so revenue keeps flowing.

For the full playbook, see debanked: how to still accept payments and, if a specific provider froze you, what to do when Stripe freezes your account.

Who gets debanked?

Far more businesses than you would think: crypto and Web3 companies, CBD and hemp, adult and creator platforms, firearms, online gaming, nutraceuticals, cross-border e-commerce, and plenty of ordinary small businesses that simply grew too fast or tripped a risk model. We break the full list down in industries most likely to be debanked.

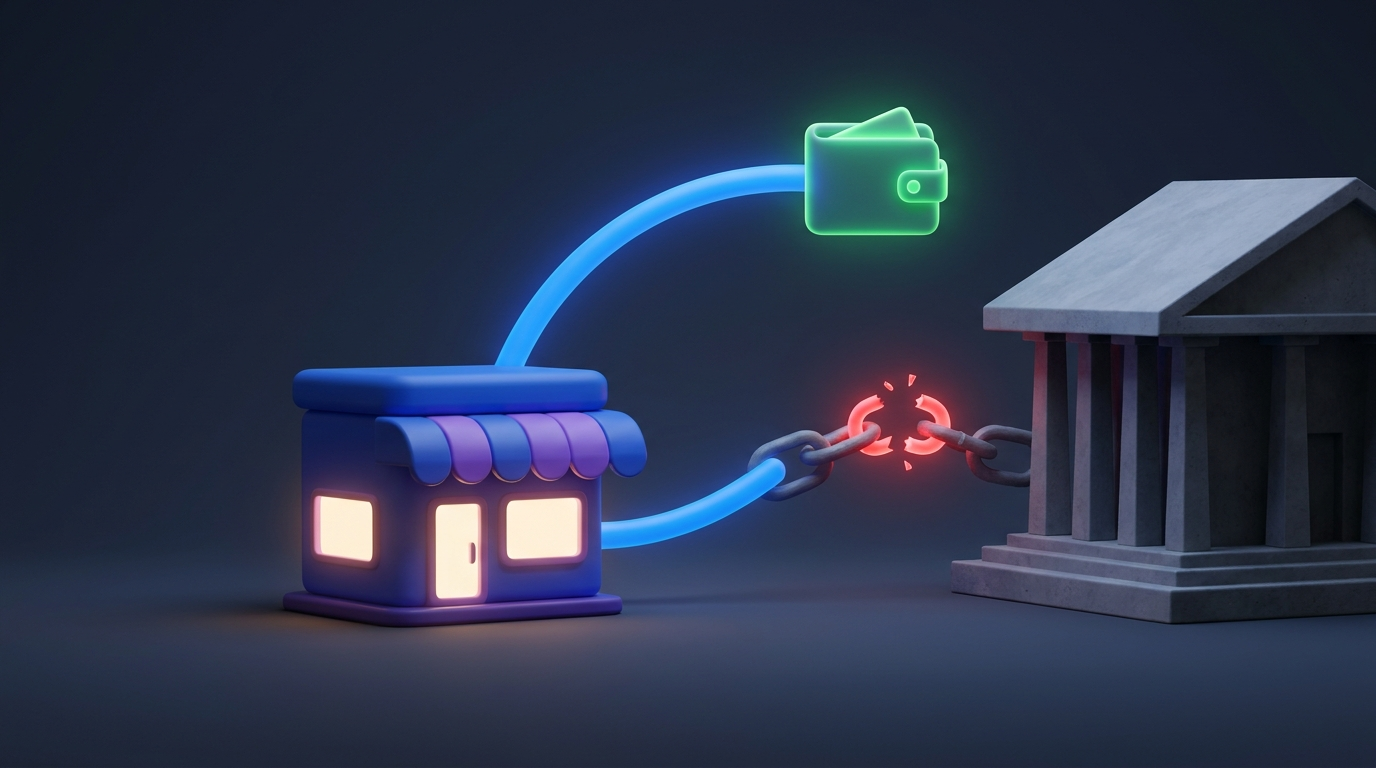

The structural fix: do not route revenue through something that can be switched off

Every debanking story shares one root cause: a third party stood between you and your money and decided you could not have it. The only way to remove that risk is to remove the third party. That is what a non-custodial crypto payment rail does — your customer pays directly into a wallet you control, with no bank or processor holding a balance to freeze.

| Bank / custodial processor | Non-custodial crypto rail | |

|---|---|---|

| Can it be switched off? | Yes | No account to close |

| Who holds your money | The provider | You, in your own wallet |

| Warning before cut-off | Often none | Not applicable |

| Risk review you can fail | Yes | None |

CryptoGate is built on exactly this: connect your own wallet via an xPub, and every payment settles straight to you. No KYC, no chargebacks, nothing for anyone to debank, and it drops into a Shopify or WooCommerce store in minutes. Most businesses run it alongside their bank as an insurance policy, so if they are ever cut off, revenue keeps flowing.

The takeaway

Debanking is not a freak event; it is a built-in feature of a system where someone else holds your money. You cannot always stop a bank from dropping you, but you can make sure it does not end your business. Add a payment rail no one can switch off.

Frequently Asked Questions

What does debanking mean?

Debanking means a bank, card processor, or payment provider ends its relationship with a customer by closing the account, freezing the balance, or refusing service, usually with little warning and no detailed reason, even though the business is legal.

Why would a bank close a legal business account?

Common reasons include anti-money-laundering compliance cost, reputational risk tied to the category, chargeback or dispute rates drifting too high, and regulatory pressure that pushes banks to exit whole sectors. The closure is usually about category risk, not wrongdoing.

Can a bank debank you without warning or a reason?

Yes. Unlike a normal closure with notice, debanking is often abrupt and opaque: a templated message and a frozen balance, with no explanation and no clear path to appeal. That opacity is why continuity planning matters.

How do I protect my business from being debanked?

Avoid routing all your revenue through a single provider that can switch it off. Add a non-custodial crypto payment rail that settles to a wallet you control, so even if a bank closes your account, there is an independent channel that cannot be frozen.

Is debanking the same as being high-risk?

They are related but not identical. Being in a high-risk category raises your odds of being debanked, but ordinary businesses also get cut off for growing too fast, tripping a fraud model, or a rising dispute rate. The fix is the same: a rail no provider can switch off.